From the Strait of Hormuz to Asian stock markets, the 2026 conflict has rattled supply chains, spiked energy costs, and left businesses worldwide navigating their most uncertain operating environment in years.

March 24, 2026 · Global Business Analysis · 10 min read

“For a long time, the nightmare scenario that deterred the US from even thinking about an attack on Iran was that the Iranians would close the Strait of Hormuz. Now we’re in the nightmare scenario.”

— Maurice Obstfeld, Peterson Institute for International Economics, former IMF Chief Economist$84

Brent crude/barrel (early March 2026), up from ~$70 pre-war

20%

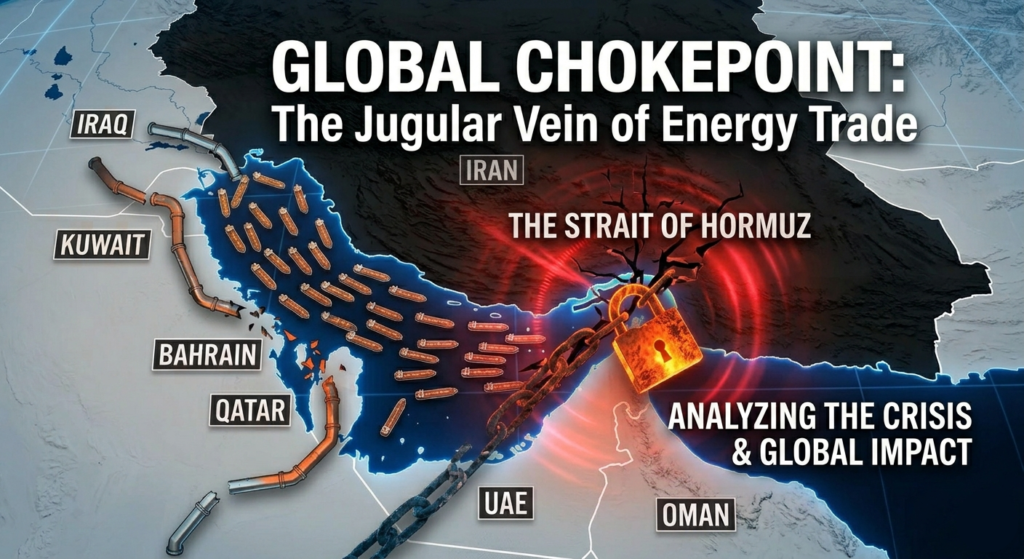

of global petroleum trade via Strait of Hormuz

−5.5%

Global stocks decline (Bloomberg)

$130+

Projected oil price in full blockade (JP Morgan)

How it started

February 28, 2026: Joint US-Israeli airstrikes kill Iran’s Supreme Leader Khamenei and senior commanders. Operation “Epic Fury” begins, targeting nuclear and military infrastructure.

March 1–8, 2026: Iran retaliates with 550 ballistic missiles and 1,000 drones. Multiple Middle Eastern countries shut airspace. Strait of Hormuz is closed.

March 2026 (ongoing): Global stocks fall 5.5%, oil surges to $84, shipping collapses, and European gas prices nearly double.

Energy: the front line for business

Iran held roughly 9% of global oil and 17% of natural gas proven reserves before the conflict. The country produced an average of 3.4 million barrels per day of crude. Within a week of hostilities, Iran’s oil exports collapsed to around 102,000 barrels per day less than half the recent average after Israeli strikes hit the Shahr Rey refinery, fuel depots around Tehran, and parts of the South Pars gas field, which provides some 80% of Iran’s gas output.

The bigger threat is the Strait of Hormuz. Through it flows roughly 20% of all global petroleum liquids. With Iran now having closed the channel, shipping activity in the region fell sharply within 24 hours of the war starting, with many vessels turning back, diverting to alternative routes, or sitting idle in the Gulf of Oman.

The IMF estimates inflation rises by nearly 0.4% for every 10% increase in oil prices. The recent jump in crude has already translated into more expensive transport fuels within days. In markets like India, Thailand, and the Philippines where energy imports drive a significant share of inflation the pass-through to transport and food prices is expected to be faster.

Impact across sectors

Aviation & Tourism

Bahrain, Iraq, Israel, Kuwait, Qatar, Syria, and the UAE closed airspace. Airlines rerouting over Afghanistan, adding journey time and fuel costs. Thousands stranded repatriation efforts described as the biggest since COVID.

Shipping & Logistics

Insurance premiums for vessels in the Strait of Hormuz have risen sharply. Freight costs rising across two major global shipping indices. Shipowners reluctant to take new orders as bunkering prices hit new highs daily.

Energy

Europe, already cut off from Russian hydrocarbons, faces a second energy crisis. Gas storage at just 30% capacity. Dutch TTF gas benchmarks nearly doubled to over €60/MWh by mid-March 2026.

Financial Markets

Asian stock markets hit hardest globally. Gold and other safe-haven assets surging. Central banks caught between hiking rates to curb energy-driven inflation and cutting to support a slowing economy.

Food & Agriculture

Higher oil-linked transport and input costs beginning to flow through food supply chains. Iran imports ~30% of its wheat; grain ships outside the Strait of Hormuz have been unable to dock.

Regional Economies

Egypt, Jordan, and Lebanon face sharp drops in tourism revenue, exports, and foreign investment. GCC growth forecasts, previously bright, are now under severe revision.

What economists are forecasting

The macroeconomic outlook depends heavily on duration. Capital Economics modelling suggests that if the war ends within a few weeks, “outside the Gulf economies, the impact on GDP, inflation and monetary policy will be limited.” But if the conflict drags on for months, the picture darkens considerably eurozone GDP growth could slow to just 0.5% year-on-year in the second half of 2026, and Chinese economic growth could fall below 3% year-on-year.

For the United States, which is energy self-sufficient, the direct exposure is lower. But petrol prices remain a political flashpoint. Evercore ISI calculates that if oil stays near $100 a barrel, higher gasoline prices would wipe out for most Americans the benefits of higher tax refunds arising from Trump’s 2025 tax cuts only the top 30% would still see a net gain.

— Eswar Prasad, Professor of Trade Policy, Cornell University

Not all economists are pessimistic. Neil Shearing of Capital Economics notes that if oil prices fall back to the $70–$80 per barrel range, “the world economy may absorb the shock with less disruption than many fear.” The world has survived the Russian invasion of Ukraine and sweeping US tariffs. Resilience, if not immunity, has been demonstrated.

The bottom line for global business

Three compounding risks now define the operating environment for multinationals: uncertainty surrounding energy flows through strategic chokepoints, complicating procurement and supply chain planning; heightened geopolitical unpredictability reducing business confidence globally; and rising volatility in shipping costs reflecting security risks and rerouting pressures.

Businesses with exposure to Middle Eastern supply chains, energy-intensive manufacturing, and transport-heavy logistics face the sharpest near-term headwinds. For boardrooms from Mumbai to Munich, the calculus is the same: prepare for an extended period of elevated energy costs, tighter margins, and supply-chain uncertainty — while watching the Strait of Hormuz very carefully.